|

browse TransFS web site for extra advice on financing 401(k) contribution limits can change every year. We’ve got the latest limits released by the IRS for 2018, as well as prior years.

401(k) plans are the primary retirement savings vehicle for the middle class. This is particularly true as more employers automatically enroll new employees in the plans. And for those who have the ability to maximize their contribution each year, the new calendar year offers an additional opportunity. In 2016 and 2017, the maximum contribution limits were the same. For retirement accounts–which include 401(k) accounts, 403(b) accounts, most 457 plans, and Thrift Savings Plans–these stayed at $18,000. In case you were holding out for an increase, I have good news: for 2018, these contribution limits will go up to $18,500. Of course, savers and investors aged 50 or older can take advantage of an additional catch-up contribution. This effectively increases the limit for those approaching traditional retirement age. In 2018, these taxpayers can contribute an additional $6,000 above the regular maximum of $18,500. As a result, if you are 50 or older, you can contribute a maximum of $24,500 into these tax-advantaged accounts in 2018. Resource: Maxed out your 401(k) or looking for better investment options? Check out an IRA at WealthFront. Total Contribution Limits and ExamplesThe total contribution limit, including employer contributions, has also changed. It is now at $55,000, up from last year’s $54,000. The benefits of a 401(k) plan are, by design, directed primarily at people who most need an incentive to save for retirement. This may help contain the tax benefits within the middle class. The government does this by applying a maximum level of compensation to which matching benefits apply. In 2017, only the first $270,000 in an employee’s compensation over the course of 2017 may be applied to the company’s matching formula. That goes up to $275,000 in 2018. That’s a sufficiently high maximum. It should cover more than just the middle class. To illustrate,say a company matches an employee’s contributions at a rate of 50% up to a limit of 5% of the salary. An employee with a $100,000 salary contributes $15,000 to her 401(k). She will receive, at most, a $5,000 matching contribution (5% of the full $100,000 salary). An employee at the same company earns $400,000 in compensation. She defers $15,000, so the matching contribution will be $13,750 (5% of the $275,000 maximum compensation, not $20,000). The IRS has additional rules that require a company to balance benefits between employees earning $120,000 or more and all other employees. Finding Account FeesBeginning in 2013, new regulations required 401(k) plan administers to explicitly state in quarterly statements how much investors are paying in fees. Previously, this information was not easy to discover. You could (and should) look at the various prospectuses in search of management expenses fees or expense ratios, expressed as a percentage of assets. But there were at least two obstacles:

Now finding those fees is easier. The regulations that started in 2013 are still in place today. Maximizing Your ContributionsTo maximize your 401(k) contribution in 2018, spread the $18,500 across the number of paychecks you plan to receive throughout the year. That’s a contribution of about $1,541 each month for those age 49 or younger. The calculation for those over 50 who want to max the contribution is about $2,041 per month. If your employer records your contributions as a percentage of your paycheck, remember to change them to account for raises and bonuses. If you are expecting your company to match your contributions at some level, and you reach your 401(k) contribution limit before your last paycheck, you may miss out on free money. The following table illustrates the change in 401(k) contribution limits over the past several years.

Take Control of Your 401kTrack and Analyze your Investments for Free: The easiest way to track and analyze all your investments, regardless of where they are located, is with Personal Capital’s free financial dashboard. By far the best financial tool we’ve ever used, Personal Capital enables you to connect all of your 401(k), 403(b), IRAs, and other investment accounts in one place. Once connected, you can see the performance of all of your investments and evaluate your asset allocation.

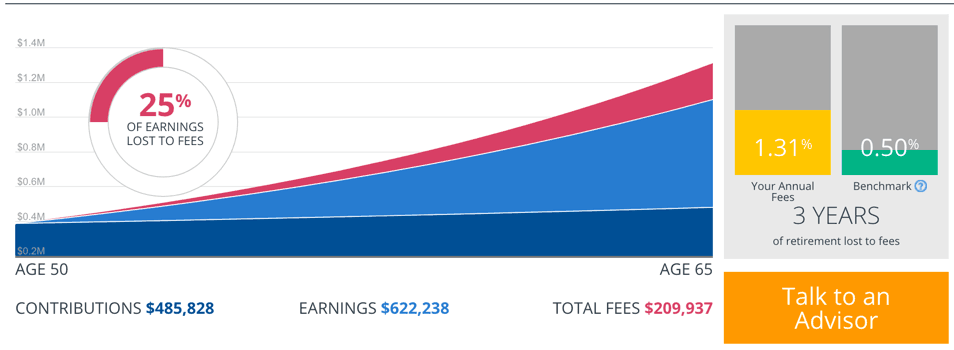

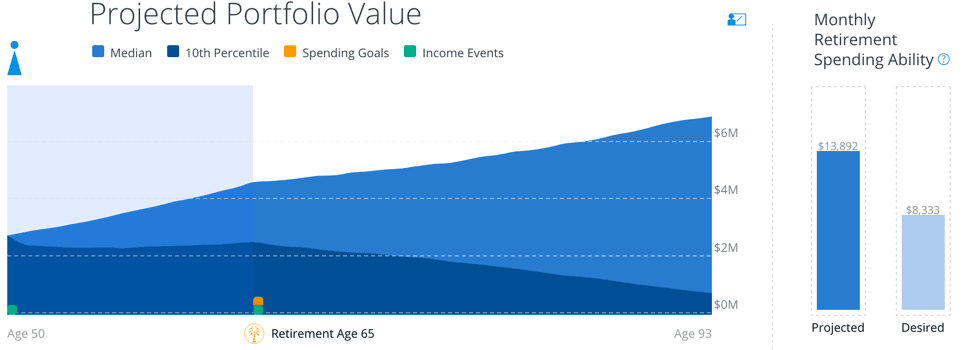

You can also see the fees you are paying through Personal Capital’s Retirement Fee Analyzer. I was stunned to learn that the fees in just my 401(k) could cost me over $200,000, requiring me to put off retirement for three years! They also offer a free Retirement Planner. This robust tool will help you plan for retirement and show you if you are on track to retire on your terms.

via billwells https://www.consumerismcommentary.com/401k-contribution-limits/

0 Comments

Leave a Reply. |

Contribution Limits")

RSS Feed

RSS Feed